Dear Prudence, The Market is Afraid

Before you know it the Holiday Season chatter will be upon us, even as the media glare on Q3 earnings makes every effort to highlight the bad stuff.

And every 48 seconds or so there will be some ridiculous update about holiday sales, to assure us all that the consumer is indeed finished…for about the 35th year in a row.

This year has had many unique roller-coaster moments already; we started with the worst five days, and worst January in 80 years, followed by a thousand predictions from Q1 onwards about how terrible 2016 would be.

We then watched as the largest intra-quarter recovery in 83 years unfolded, which was then quickly abandoned for Brexit, Branic and any number of other portmanteaus for Britain’s vote to leave the EU.

And of course the world was expected to end.

But it didn’t, again. The markets staggered for about 24 hours and then Armageddon was over.

Rate Hike Apocalypse (RHA)

But the media wasn’t done yet. The fear of a 25-basis point hike in interest rates was locked in on as nightmarish option, one certain to fell an $18++Trillion economy call the United States.

Yet that overblown fear has shaved gains this year for the Dividend Growth Investor audience and has reset prices.

Obviously, these fears come and go, companies adjust, prices fall back and then value buyers come in for the yield, which after price setbacks the market is already working in the potential rate hike before the year’s end.

Let me be the first to assure you of this: If the Fed does not raise rates and the earnings season turns for the better as it appears to be doing, then by the middle of 2017 (maybe sooner) the very same crowd of experts terrifying you about rate hikes today, will instead be howling at the same moon; snarling that the Fed is now behind the curve because we are growing too fast for low rates to stay intact.

The Fed’s real fight is with a monster far larger than America’s economy. It’s fighting a mind-set of fear so deeply imbedded that the masses will deny it for many thousands more Dow Jones points.

And they will push back by redefining their fear as prudence.

This will likely continue even as the cash piles up in banks, the demand for cash remains at record highs and they stand in line to buy bonds at 1.75%, or even 2.00% after rate-fear-induced selling.

Why?

In the current storm of fear, 2.00% for ten years is, after all, better than the 1.45% they were standing in line to buy 30 days ago, right?

And we complain about a stock raising dividends for 40 or 50 years straight starting with a yield twice that high!

The Beat Goes On....

I stand by the idea that market chop is king until the US election has been decided.

And as much as I love stock market bounces, the latest one is on the back of half the crowd missing with the bond market closed. That means light trade is nearly assured; bounces generally don't live in that environment.

Besides, the earnings season kicks off now and man oh man, I have a feeling this will be one for the ages.

It has been my experience that troughs and turns in earnings trends are almost always ugly as the parties fighting for ground in the game will slice and dice every element of a report, even making up stuff to fill in the cracks if they need to in order to stick to their perspective.

Vote for the correction, I say. A washout for more value resets would not be such a terrible thing.

In fact, it may finally convince anyone running for President that it’s our fiscal policy that’s forcing this economic walk through quicksand.

Doing a better job in Washington DC to benefit business and future investment incentive, the lifeblood of jobs and growth, should be priority one now. That’ and taking away the chains draped over the economy over the last eight years and you’ll soon see a miraculous shifting of gears while we climb to higher growth levels.

And Speaking of Holidays...

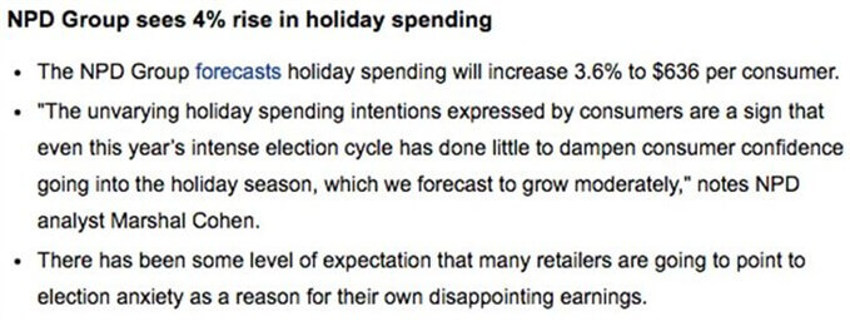

Here is the latest projection from the retail quants who count numbers on all of our receipts in store or at online websites we collectively visit and do business with:

We Shall Survive

Even from the guys who should know best, we’re hearing that we’re not likely to see terrible things unfold.

Sure, the election will get uglier, but as Dr Ed Yardeni always says, “When things get tough we go shopping.”

Jobs Friday Was Ho-Hum?

Not so fast. Our problem is not lack of jobs. Our problem is lack of people.

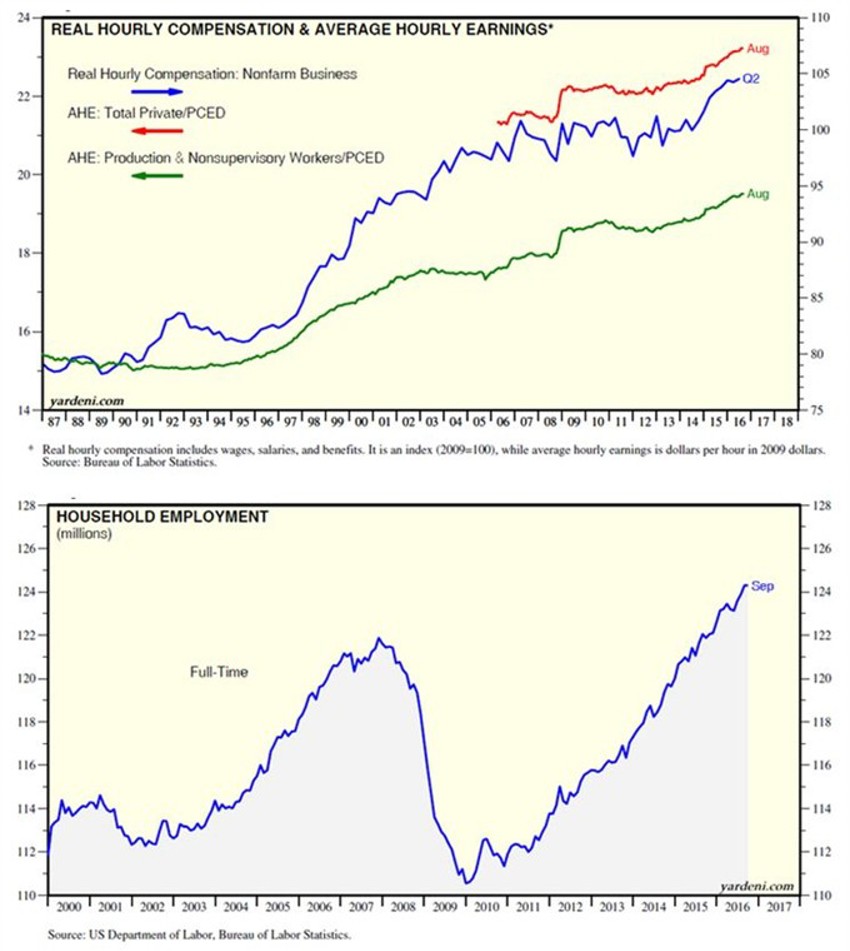

Let's go over a few items real quick with the help of few great charts from Dr Ed and his team:

Contrary to the always-feared myth (driven by countless experts in the press) that real wages have stagnated for the past 15-20 years, average hourly earnings divided by the headline PCED rose to a record high during August!

For all workers that figure is up 1.4% year-on-year, and 8.9% since the start of the data during March 2006. For production and nonsupervisory workers, this measure of real hourly pay rose 1.5% year-on-year and 13.5% over the past 15 years (since August 2001).

The other good news in Friday’s report?

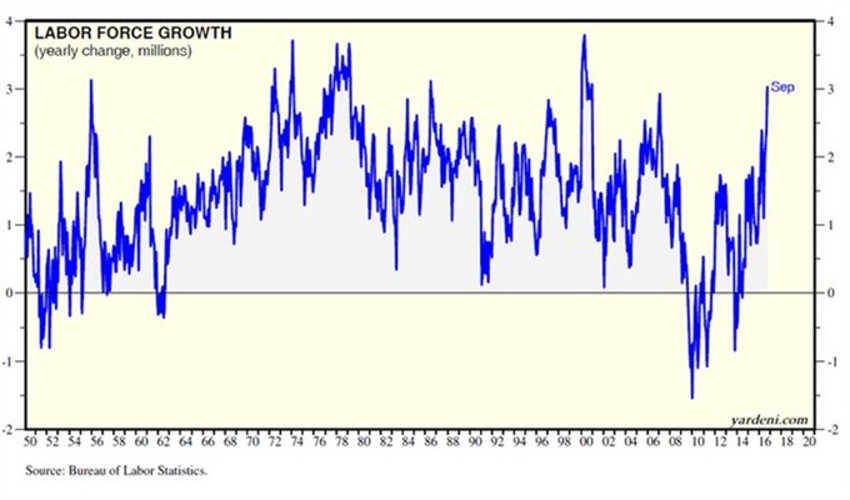

Well, the US labour force rose 444,000 and household employment gained 354,000. The labour force has increased 3.0 million over the past 12 months versus being up 738,000 during the previous 12 months. It was the best such gain since December 2000 and closing in on levels not seen since the late 1970s / early 1980s when the Baby Boomers first joined the economic fray; just as Generation Y is now.

The household measure of employment is also up 3.0 million over this same period, the best performance since February 2015.

And last but not least; the number of full-time workers is at new a record high of 124.3 million!

Just keep in mind that:

- This feeling of going nowhere is actually the early stage of change. The baton is passing. Change is being brought to us by the record-breaking size of Millennials generation here in the US, and

- Too many investors forget that markets generally do not act on what's now; they act on what's next.

Consumer Health?

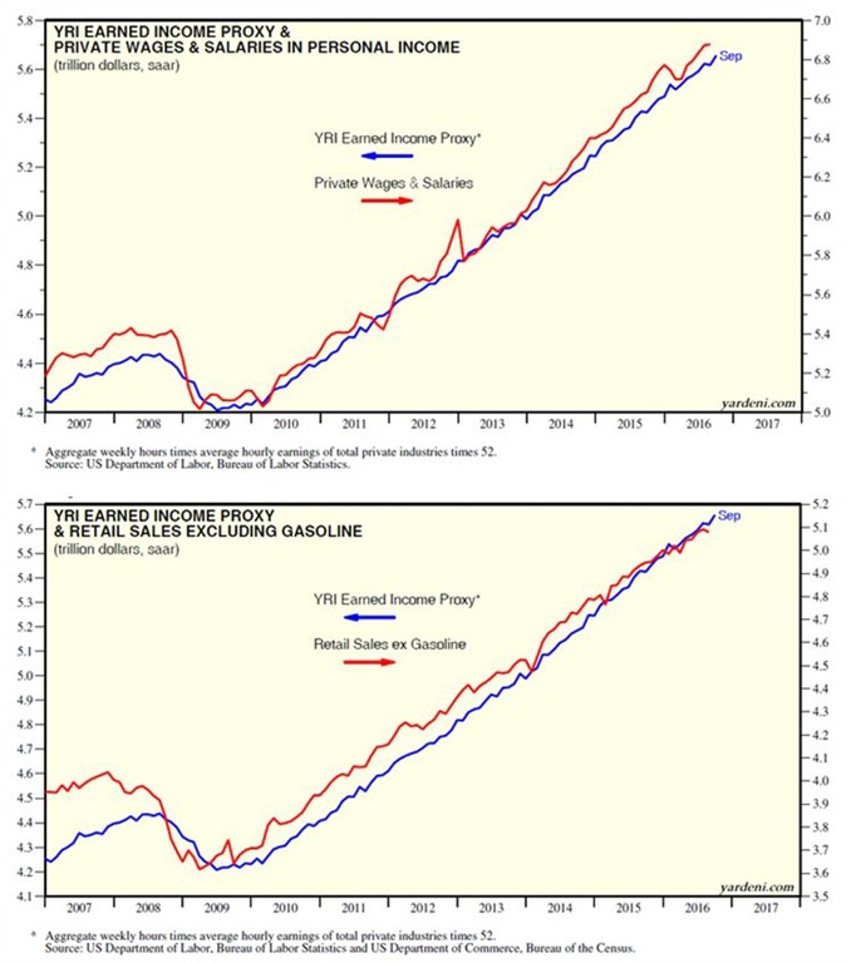

The last important element for today that we can pull from the employment data on Friday is this: The consumer is healthy, income is up and there’s steady support ahead for retail sales:

As the two charts above show you, the data remains positive for both personal income and spending; with each continuing to rise into record high territory.

Dr Ed's Earned Income Proxy (EIP) rose 0.6% month-on-month to a new record high. This is a proxy for the private sector’s wages and salaries - the largest component of personal income.

It’s also highly correlated with retail sales, excluding gasoline.

Don't be surprised if Ms. Yellen gets to the holiday season and thinks aloud to the Federal Reserve Board, “Why tinker now?”

The Bottom Line

Longer-term market chop is your friend, as is maybe even a week or two of correction.

After the election our view remains that surprises will be to the upside.

Be patient, stay focused and stick to your plan.

And finally; think demographics, not economics. We are in great shape with a solid future ahead and plenty of potholes to work around.